Where's the inflation?

The Sunday press ponders about why the extraordinary expansion of the monetary base by the SNB was not followed by runaway inflation. The author meets with his former professors and gets basically three answers, that is three that caught my eye: (i) wait-and-see, inflation will come; (ii) there are special factors such as China and the free movement of persons that keep Swiss inflation low; (iii) macro has failed us as textbooks do not manage to explain what we see.

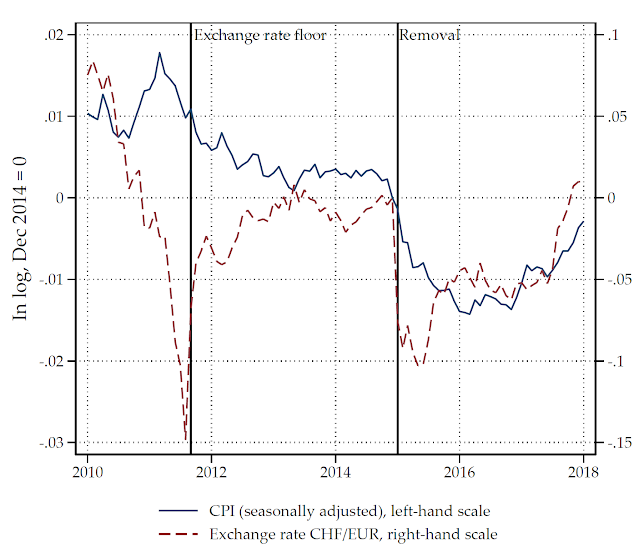

I disagree on all three points. On the first and third point, I wrote extensively about why inflation has come down and why low inflation can be consistent with a large balance sheet (see here, here, and here). Note that all the arguments in these posts are consistent with standard international finance and monetary macro textbooks. Nowadays, they treat the liquidity trap not as a Japanese pecularity but feature it much more prominently. But, the theoretical knowledge was of course available before the financial crisis. Krugman's liquidity trap argument made 20 years ago goes a long way of explaining what we actually see (and the "New Keynesians" that emphasize the importance of liquidity trap economics are actually modern Monetarists).

In addition, articles like these often refer to monetarism as a school of thought claiming that an increase in the (growth rate of) money supply is always followed by an increase in inflation. This is false. Friedman and Schwartz, in their Monetary History of the United States, analyzed very carefully actions by the central banks that affect money supply, but also, money demand. One example is that they observe that the Federal Reserve increased reserve requirements in the Great Depression, which was one factor exacerbating the crisis. Reserve requirements, however, increase first and foremost money demand because banks have to hold more central bank reserves. In this sense, they were perfectly aware that money demand can be unstable if the central bank changes its operating framework. But as long as the central bank does not meddle with money demand it would be sufficiently stable to control the money supply and ultimately control inflation. The experience of Japan, and the work of Krugman, then showed that money demand can become highly unstable when interest rates fall to zero and therefore monetary policy looses its traction. When interest rates are zero, demand is declining with the quantity of money because I would rather invest my money in an asset that yield a positive interest rate. If interest rates are zero (or negative) anyway, I am perfectly happy to hold money that also yields a zero (or negative) interest rate. So the central bank can expand the money supply strongly without having a strong effect on economic activitiy and inflation.

The third point actually is not about inflation at all. The special factors (the impact of labor mobility on wages, the impact of Chinese products on imported goods prices) are about real wages and real prices, that is adjusted for inflation. Economists sometimes talk about relative price movements (that is relative to some sort of aggregate price level); these relative price movements have nothing to do with inflation. For example, computers become cheaper, train tickets more expensive. But this does not mean that computer prices signal deflation and train ticket prices inflation. Actually, computer prices fall relative to other prices and train tickets rise relative to other prices. If we have positive inflation at the same time, this means that computer prices would fall more if there was no inflation; and train ticket prices would rise less if there was no inflation. Again, this is standard macro.

To sum up, for the moment I feel very comfortable teaching macro and international finance with the textbooks available (next week the semester starts with macro-économie 2 and international finance). I do not find it very difficult to relate the theories to the developments that we see. I hope I will be able to convince my students as well.

I disagree on all three points. On the first and third point, I wrote extensively about why inflation has come down and why low inflation can be consistent with a large balance sheet (see here, here, and here). Note that all the arguments in these posts are consistent with standard international finance and monetary macro textbooks. Nowadays, they treat the liquidity trap not as a Japanese pecularity but feature it much more prominently. But, the theoretical knowledge was of course available before the financial crisis. Krugman's liquidity trap argument made 20 years ago goes a long way of explaining what we actually see (and the "New Keynesians" that emphasize the importance of liquidity trap economics are actually modern Monetarists).

In addition, articles like these often refer to monetarism as a school of thought claiming that an increase in the (growth rate of) money supply is always followed by an increase in inflation. This is false. Friedman and Schwartz, in their Monetary History of the United States, analyzed very carefully actions by the central banks that affect money supply, but also, money demand. One example is that they observe that the Federal Reserve increased reserve requirements in the Great Depression, which was one factor exacerbating the crisis. Reserve requirements, however, increase first and foremost money demand because banks have to hold more central bank reserves. In this sense, they were perfectly aware that money demand can be unstable if the central bank changes its operating framework. But as long as the central bank does not meddle with money demand it would be sufficiently stable to control the money supply and ultimately control inflation. The experience of Japan, and the work of Krugman, then showed that money demand can become highly unstable when interest rates fall to zero and therefore monetary policy looses its traction. When interest rates are zero, demand is declining with the quantity of money because I would rather invest my money in an asset that yield a positive interest rate. If interest rates are zero (or negative) anyway, I am perfectly happy to hold money that also yields a zero (or negative) interest rate. So the central bank can expand the money supply strongly without having a strong effect on economic activitiy and inflation.

The third point actually is not about inflation at all. The special factors (the impact of labor mobility on wages, the impact of Chinese products on imported goods prices) are about real wages and real prices, that is adjusted for inflation. Economists sometimes talk about relative price movements (that is relative to some sort of aggregate price level); these relative price movements have nothing to do with inflation. For example, computers become cheaper, train tickets more expensive. But this does not mean that computer prices signal deflation and train ticket prices inflation. Actually, computer prices fall relative to other prices and train tickets rise relative to other prices. If we have positive inflation at the same time, this means that computer prices would fall more if there was no inflation; and train ticket prices would rise less if there was no inflation. Again, this is standard macro.

To sum up, for the moment I feel very comfortable teaching macro and international finance with the textbooks available (next week the semester starts with macro-économie 2 and international finance). I do not find it very difficult to relate the theories to the developments that we see. I hope I will be able to convince my students as well.

Comments

Post a Comment